Acquisitions & Partnerships:

Acquisitions and partnerships have been key to expanding our multi-beverage platform in core markets, driving significant growth and value creation. The foundation of any acquisition is its alignment with our operating model and its potential to deliver synergies. Our strengthened platform has positioned us as a more robust and attractive partner.

Acquisitive growth

Since 2021, acquisitions have contributed with DKK 4.7bn annual net revenue, equivalent to more than half of the growth in the period. The majority comes from platform acquisitions (please see next page for an explanation of different types of acquisitions). In general, platform acquisitions require longer time for synergies to be realized compared to other types of acquisitions. Usually, they also require investments in equipment, capabilities, and organizational capital, and a culturalshift before synergies start to manifest. However, historically, platform acquisitions have also been the ones to provide the most significant value creation over time.

On October 16, 2024, we signed an agreement to acquire Pernod Ricard’s portfolio of local Nordic brands within spirits, liqueurs and local wine brands. The most well-known brand is Minttu, a leading liqueur brand in Finland which is also exported to few countries nearby Finland. The transaction is expected to be finalized by the end of February 2025.

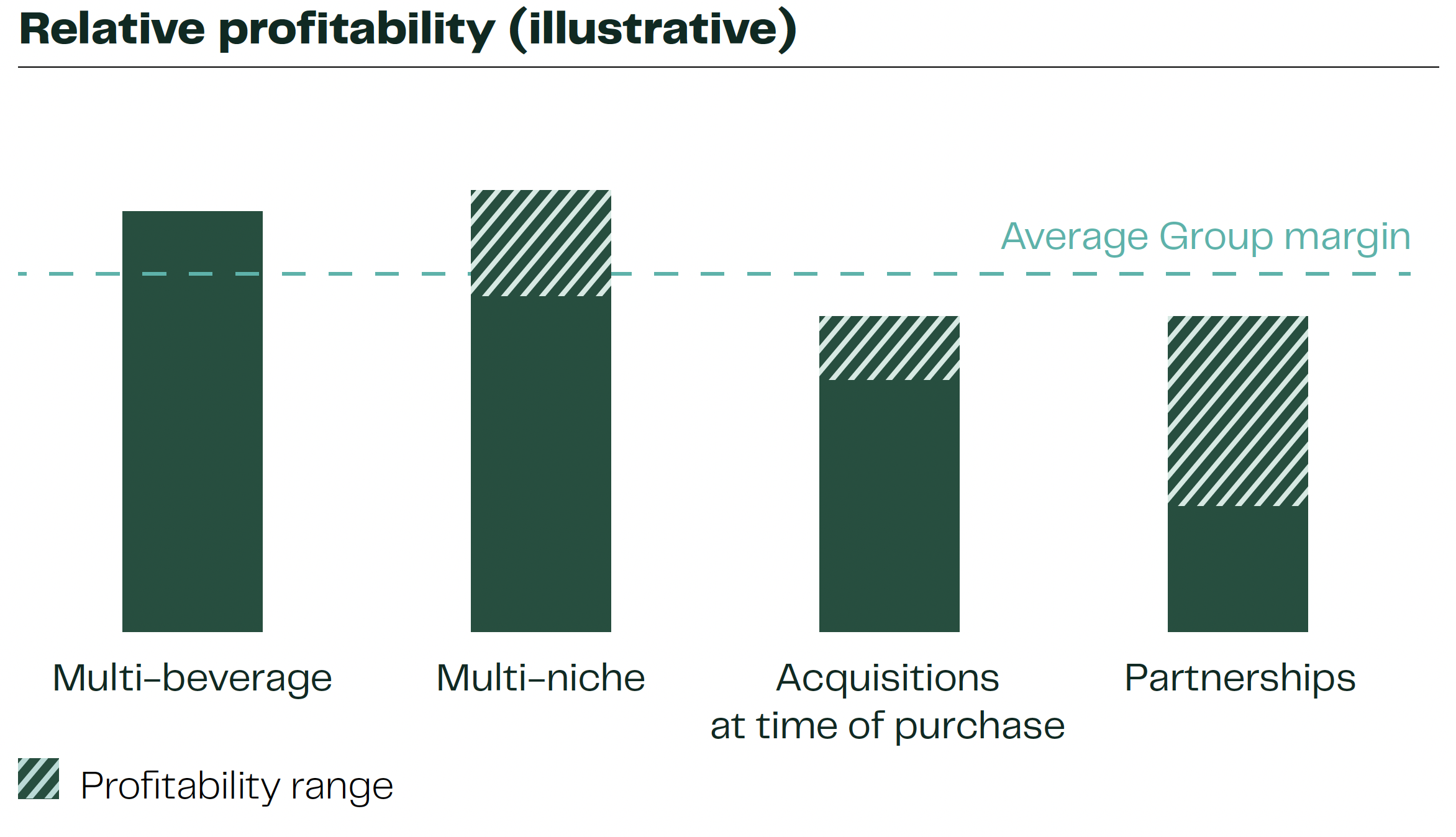

Acquisitions add revenue and earnings but typically come with lower margins, as our legacy margins are positioned at the high-end of the beverage sector. Thus, the acquisitions we have made in recent years have diluted our EBIT margin by approximately 5 percentage points. It is our clear goal and priority to enhance the profitability of acquired businesses and improve margins over time. As an example, Solera Beverage Group (acquired in 2021) is a distribution business, which is notexpected to be able to deliver margins at Group level, however, capital employed is relatively low.

Growth through partnerships

We have significantly expanded our partnerships in recent years. In 2024, we took over PepsiCo’s beverage business as well as the field sales activities of PepsiCo’s snack portfolio in Belgium and Luxembourg. We have established an organization of more than 60 people in Belgium to run the operations.

Our partnership with PepsiCo include the snack portfolio in all Nordic countries as well as the beverage business in Finland and Denmark, which also includes the beverage business on the border between Denmark and Germany.

In recent years, we have also extended our collaboration agreement with Diageo to include the Norwegian market, along with several additional new partnerships. The profitability of these partnerships varies depending on whether they are solely based on distribution or also involve production, sales, and marketing.

As a starting point, partnerships are dilutive to the EBIT margin. In general, the capital employed is low, which makes the return on invested capital very attractive. Additionally, it enhances our product portfolio with strong brands that further support the sales of our own products.

As a result of acquisitions and partnerships, Royal Unibrew has transformed into a Nordic multi-beverage company with a significant presence and multiple platforms in Western Europe with ample opportunities to drive future organic growth.

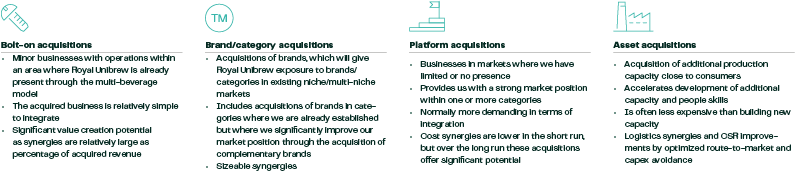

Types of Acquisitions

Over the past four years, we have made several acquisitions that have contributed to enhancing our multi-beverage platform and to expanding and optimizing our capacity utilization. No acquisitions were finalized in 2024.

We categorize acquisitions into four different types.